Pakawadee Wongjinda/iStock via Getty Images

By Garey J. Aitken, CFA | Michael Richmond, CFA

Energy reversal caps off 2024 – Q4 2024

Market overview

North American stocks ended 2024 on a strong note. The S&P 500 and S&P/TSX Composite Index generated positive total returns of 9.1% (CAD) and 3.8%, respectively, in the fourth quarter of 2024.

While both major stock indexes were higher, the underlying economic backdrop for Canada and the United States remains divergent. In the United States, Donald Trump’s re-election and Republican sweeps of both houses of Congress have cleared the way for a series of pro-business policies that have stirred up animal spirits in markets. Strong GDP and employment growth, as well as inflation that continues to be above target, led the Federal Reserve to adopt a more hawkish tone in its December policy release, reflecting the strength of the U.S. economy.

In comparison, Canada’s economy will continue to show signs of weakness in 2024, with GDP and employment growth remaining sluggish. The threat of tariffs from the incoming U.S. administration, combined with slower population growth as the federal government tries to ease the burden on strained public services, has diverged economic prospects for Canada and the United States.

The differing outlook reflects a very weak quarter for the Canadian dollar. The Canadian dollar fell 6%, reflecting the different expected paths of monetary policy (a more hawkish Fed and a more dovish Bank of Canada) and threats to the Canadian economy in 2025. The lowest levels outside of the pandemic since 2015.

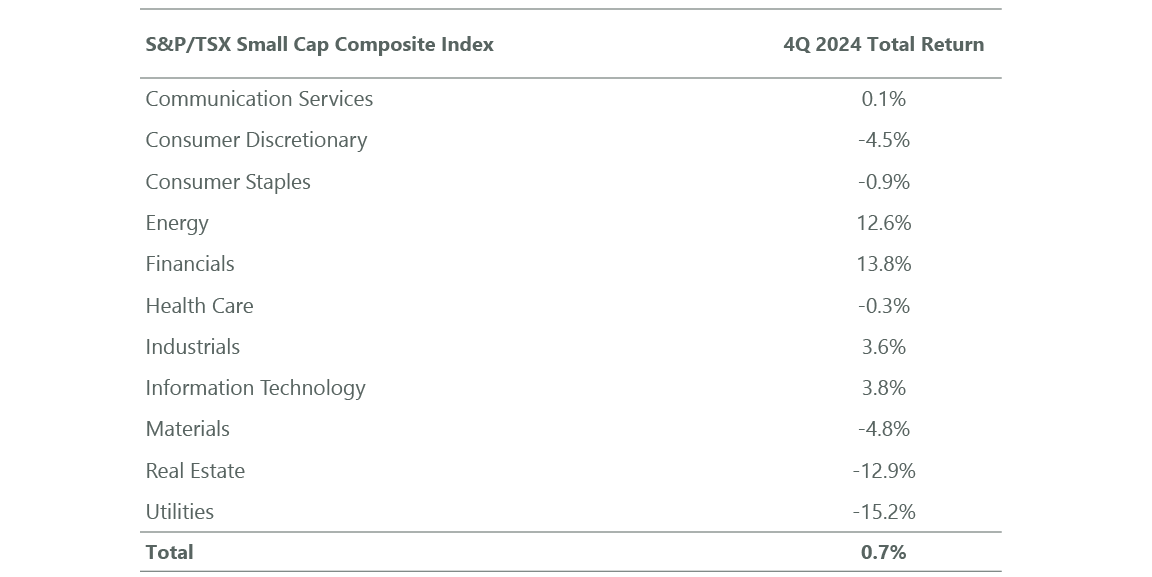

The S&P/TSX Small-Cap Total Return Index lagged the large-cap index in the fourth quarter, rising just 0.7%. The small-cap index moved higher, led by financials (+13.8%) and energy stocks (+12.6%), while the more rate-sensitive utilities (-15.2%) and real estate stocks (-12.9%) lagged significantly on the benchmark index. Weaker gold prices, partly due to rising interest rates, sent the heavily weighted Materials sector (-4.8%) lower.

Contrary to what happened last quarter, the energy industry was the largest contributor to the benchmark’s overall performance in the fourth quarter, and the materials industry was the biggest drag. Energy was supported by strength in WTI crude oil, which rose 5.2% for the quarter to $71.72/barrel, and NYMEX natural gas prices, which rose 24.3% (albeit from a low base) to $3.63/mmbtu. The oilfield services subgroup continued to perform well despite a sharp decline in the North American rig count during the quarter.

Rate-sensitive utilities and real estate sectors underperformed the benchmark. Long-term interest rates have moved higher this quarter despite both the Bank of Canada and the Federal Reserve lowering policy rates. The Canadian government’s 10-year government bond yield rose 28 basis points to 3.23% at the end of the quarter, and the U.S. 10-year government bond yield rose 84 basis points to 4.57% at the end of the quarter.

Exhibit 1: Small Cap Performance by Industry

Ends December 31, 2024.

ClearBridge’s Canadian small-cap strategy outperformed its benchmark during the quarter. Overweight Energy and Financials, Underweight Materials, and strong stock picks in Energy, Consumer Staples, and Materials were the primary sources of outperformance.

In the energy sector, strong quarterly results from Enerflex (EFXT), Parex Resources (OTCPK:PARXF) and Kelt Exploration (OTCPK:KELTF) delivered meaningful positive selection effects. Enerflex delivered stellar quarterly results, growing 78% amid a positive natural gas macro backdrop, which combined with operational stability, debt reduction, modest dividend growth and a severely depressed valuation set the stage for outsized stock returns. Parex partially recovered from weakness in the third quarter, while Kelt benefited from higher natural gas prices.

The only significant drag on relative performance this quarter was the information technology (IT) industry. Shares of Converge Technology Solutions ( OTCQX:CTSDF ) fell 29%, weighed by mixed third-quarter results and 2025 outlook, while Sylog ( OTCPK:SYZLF ) also significantly underperformed.

Portfolio positioning

Volatility kept us active in the quarter. We eliminated two positions and added two new names to the portfolio, actively adjusting weights as opportunities arise.

After strong growth, we eliminated our position in Security Energy Services. Secure has successfully pivoted its business from traditional oilfield services valuations to industrial valuations, which we believe fairly reflects the energy volatility and earnings stability of its waste-oriented business lines. We also eliminated our position in Dexterra Group ( OTCPK:HZNOF ) and saw better risk-reward opportunities in other stocks.

This quarter we added two new materials investments to our portfolio – Hudbay Minerals (HBM) and Capstone Copper (OTCPK:CSCCF) – and added to our position in Lundin Mining (OTCPK:LUNMF). Hudbay and Capstone are both mid-sized copper producers with substantial existing operations and growth potential, with appropriate balance sheets and improving free cash flow positions.

In the case of Capstone, the business combination with Mantos Copper created a rapidly growing copper company with a stronger management and operating team. Meanwhile, Hudbay has recently shown improvements in operating performance as it continues to advance its Copper World project. Both companies trade at attractive levels in terms of our assessment of the intrinsic value of the businesses and have excellent selectivity on the long-term theme of accelerating electrification.

We trimmed several positions to build strength and reallocated gains to other opportunities. These include Bird Construction (OTCPK:BIRDF), Enerflex, and TransContinental (OTCPK:TCLAF), all of which posted a series of positive operating results and earnings updates during the quarter that drove stocks to recent highs, as well as Canadian Western Bank (OTCPK:TCLAF).

We added positions in Richelieu Hardware ( OTCPK:RHUHF ), Parkland ( OTCPK:PKIUF ), Converge Technology Solutions, InterRent REIT ( OTC:IIPZF ) and Headwater Exploration ( OTCPK:CDDRF ). We view these companies as a collection of high-quality companies that have been negatively impacted by a range of circumstances and where current valuations do not reflect the fair value of the business.

prospect

Our investment approach is a bottom-up strategy that prioritizes identifying and exploiting market inefficiencies using time arbitrage resulting from our proprietary research and long-term investment horizons. This approach is supported by our patient culture, allowing us to make informed decisions when there is a discrepancy between expectations and underlying principles. We are unwaveringly committed to our investment style and tirelessly seek out businesses that have smart capital allocation practices, enjoy structural competitive advantages, are able to generate high-quality growth and achieve this with the appropriate capital structure.

We believe that high-quality growth companies with appropriate capital allocation policies and capital structures should be well prepared to deal with tariff-related uncertainties and adapt to the pace and direction of monetary policy. Additionally, we believe these companies should be well-positioned to proactively improve their competitive position in volatile markets.

Portfolio Highlights

ClearBridge’s Canadian small-cap strategy significantly outperformed its benchmark in the fourth quarter. In absolute terms, the strategy generated returns in five of the nine industries it invested in (11 in total). The main contributors to absolute returns were the energy and financials sectors, while real estate was the main drag.

Relative to the benchmark, overall security selection and sector allocation were positive. The strategy was positively influenced by overweighting the energy sector and underweighting the materials sector. Stock selection was also positive in energy, utilities, materials and consumer staples. On the downside, stock picks in IT and financial stocks and overweight on utilities weighed on the performance.

Among individual securities, the leading absolute contributors are Enerflex, Parex Resources, Propel Holdings (OTCPK:PRLPF), Macetex (MEOH), and Descartes Systems Group (DSGX). Individual critics include Converge Technology Solutions, Real Matters (OTCPK:RLLMF), Sylogger, InterRent REIT and Boralex (OTCPK:BRLXF).

|

Past performance is no guarantee of future results. Copyright © 2024 ClearBridge Investments. All opinions and data contained in this review are as of the date of publication and are subject to change. The views and opinions expressed herein are solely those of the author, may differ from those of other portfolio managers or the firm as a whole, and are not intended to be a prediction of future events, a guarantee of future results, or investment advice. This information should not be used as the sole basis for making any investment decisions. Statistics are obtained from sources believed to be reliable, but the accuracy and completeness of the information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses resulting from the use of this information. Source of performance: Internal. Benchmark source: Standard & Poor’s. |

Original post

Editor’s note: Summary highlights for this article were selected by Seeking Alpha editors.

")